Commercial real estate lending lives and dies by one number: the Debt Service Coverage Ratio. Every commercial mortgage application, every bridge loan term sheet, every CMBS securitization — they all come back to DSCR. Yet most borrowers (and plenty of junior analysts) don't fully understand how it's actually calculated.

What DSCR Actually Measures

DSCR answers a deceptively simple question: Can this property's income cover its debt payments?

A DSCR of 1.00x means the property generates exactly enough income to cover loan payments — zero margin. Most commercial mortgage lenders require 1.20x–1.25x minimum. DSCR loan programs designed for investors typically accept 1.00x, sometimes lower with rate adjustments. According to the OCC Comptroller's Handbook on Commercial Real Estate Lending, lenders should establish minimum DSCR thresholds as part of their CRE credit risk management framework.

Simple formula. The complexity is in what goes into each side.

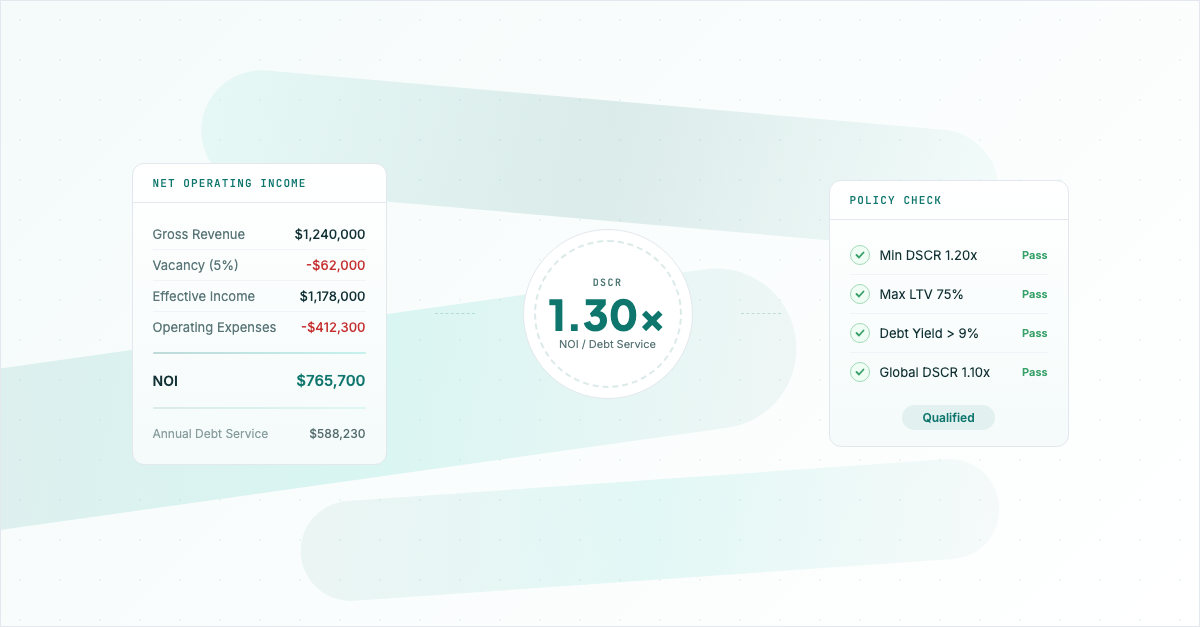

Step 1: Build the Revenue Picture

Gross Potential Rent (GPR)

Start with the rent roll — every unit, every lease, what they're paying, when their lease expires. But underwriters don't just take face-value rent. They stress it:

- In-place rents — what tenants are actually paying today

- Market rents — what comparable properties are getting (pulled from CoStar, REIS, or local comps)

- The lower of the two — conservative underwriters use the lesser for each unit. If a tenant is paying $2,200/mo but market is $1,900, they'll often use $1,900, assuming that rent won't hold at renewal.

For DSCR loans on 1–4 unit investment properties, lenders typically use a single-point estimate from an appraisal's income approach or a 1007 rent schedule.

Vacancy and Credit Loss

Nobody runs at 100% occupancy forever. Underwriters apply:

- Physical vacancy — typically 5–10% even for stabilized properties, regardless of current occupancy

- Credit loss — an additional 1–3% for tenants who don't pay

- Economic vacancy — concessions, free rent periods, lease-up costs

A property sitting at 98% occupied today still gets underwritten at 90–95% effective occupancy. Lenders aren't underwriting today's snapshot — they're underwriting the loan term.

Other Income

Parking fees, laundry, late charges, application fees, pet rent, storage. These count, but underwriters haircut them aggressively — often by 20–30% — because they're less predictable than base rent.

Step 2: Calculate Operating Expenses

This is where borrowers and lenders diverge the most. Borrowers report what they spent. Underwriters calculate what it costs to operate the property sustainably.

The Major Categories

| Expense | Typical % of EGI | Notes |

|---|---|---|

| Property taxes | 8–15% | Use actual tax bill, stress for reassessment at purchase price |

| Insurance | 3–6% | Trending up sharply — get an actual quote |

| Management fee | 5–10% | Charged even if self-managed |

| Repairs & maintenance | 5–10% | Age-adjusted — a 1970s garden apartment isn't 2% |

| Utilities (owner-paid) | 3–8% | Only if not tenant-paid |

| Replacement reserves | $250–$500/unit/yr | Capital expenditure reserve — roofs, HVAC, parking lots |

The Self-Management Trap

Borrowers who self-manage love to claim "no management expense." Underwriters add one anyway — typically 5–8% of EGI. Why? Because the loan outlives the borrower's willingness to manage. If you get hit by a bus, someone's paying a property manager. The property must support that.

Replacement Reserves

This is the expense borrowers argue about most. Replacement reserves aren't an actual cash outflow — they're an underwriting convention that says: roofs need replacing, parking lots need repaving, and the DSCR needs to account for that.

Typical reserves: $250–$500/unit/year for multifamily. Higher for older properties. Some CMBS underwriters use engineering report reserve estimates instead of flat assumptions.

Step 3: Size the Debt Service

Annual debt service is straightforward math — but the inputs matter:

- Loan amount — usually constrained by the lower of LTV or DSCR (you solve both ways and take the smaller number)

- Interest rate — for adjustable-rate loans, most underwriters stress at a 2% rate cushion above the start rate, or use the fully indexed rate, whichever is higher

- Amortization period — 25 or 30 years for permanent loans; interest-only for bridge loans

- Loan term — often shorter than amortization (10-year term, 30-year am = balloon payment at maturity)

For construction loans, DSCR is typically calculated on the projected stabilized NOI against the permanent financing that will take out the construction loan — not against the construction loan itself.

Step 4: The DSCR Calculation

But that's just the property-level DSCR. Most SBA lenders and community banks also run a global analysis.

Global DSCR (aka Global Cash Flow)

Property NOI alone doesn't tell the whole story. Global DSCR includes:

- Property NOI

- Borrower's other real estate NOI (all properties)

- Personal income (W-2, K-1, Schedule C)

- Personal debt obligations (mortgages, auto loans, credit cards)

- Business debt from related entities

This is why SBA 7(a) and SBA 504 deals scrutinize personal tax returns — they're building a global cash flow picture.

Stress-Tested DSCR

Sophisticated lenders (especially CMBS shops) also run stress scenarios:

- Rate stress: What's DSCR at current rate + 200bps?

- Vacancy stress: What if occupancy drops to 80%?

- Expense stress: What if insurance doubles? (Not hypothetical in 2025–2026.)

- Combination stress: All of the above simultaneously

If the deal breaks below 1.00x under any reasonable stress scenario, expect tighter terms or a decline.

Step 5: The Credit Decision

DSCR isn't pass/fail — it's a spectrum:

| DSCR | What It Means |

|---|---|

| < 1.00x | Property doesn't cover debt. Most lenders won't touch it. Some DSCR programs allow it with rate premiums. |

| 1.00x–1.10x | Thin. Expect higher rates, lower leverage, or additional collateral. |

| 1.10x–1.20x | Acceptable for many hard money and bridge lenders. |

| 1.20x–1.25x | The sweet spot for commercial mortgages. Standard institutional threshold. |

| 1.25x–1.50x | Strong. You'll get competitive terms and lender interest. |

| > 1.50x | Excellent. You have leverage to negotiate on rate, structure, and recourse. |

But DSCR is just one constraint. The final loan amount is the lowest of:

- Maximum LTV (e.g., $5M value × 75% = $3.75M)

- Maximum DSCR-constrained amount (solve for loan amount where DSCR = minimum)

- Maximum dollar exposure for that asset class

- Maximum debt yield threshold (NOI / Loan Amount, typically 8–10%+)

The binding constraint wins. On most deals, it's either LTV or DSCR.

Where This Process Breaks Down

Here's the honest truth: this entire analysis — from rent roll to credit decision — is largely manual at most banks and lenders. Analysts pull rent rolls from PDFs, key in expenses from tax returns, manually check lease expirations against market comps, build Excel models, and write credit memos that repeat 80% of the same language as the last deal.

It works, but it's slow. A typical commercial mortgage underwrite takes 2–6 weeks from application to credit committee. Half that time is spent on data extraction and spreading, not actual analysis.

How AI Is Changing CRE Underwriting

This is exactly the problem Aloan is solving. AI-powered underwriting doesn't replace the credit judgment — it eliminates the manual data work that buries analysts:

- Automated document extraction — rent rolls, operating statements, tax returns, and appraisals parsed in seconds instead of hours

- Intelligent spreading — expenses automatically categorized, normalized, and compared to benchmarks

- DSCR calculated in real time — as documents are ingested, the model updates. No waiting for an analyst to finish the Excel

- Global cash flow assembly — personal and entity-level income and obligations pulled from tax returns automatically

- Anomaly detection — flags when reported expenses deviate from market norms, when rent rolls don't reconcile with bank statements, when something doesn't add up

The credit officer still makes the decision. But instead of getting a package 3 weeks later, they get a complete, verified analysis in hours. The underwriter's job shifts from data entry to judgment — which is where it should've been all along.

If you're a lender evaluating how AI fits into your CRE underwriting process, see what Aloan is building.

FAQ: DSCR underwriting for commercial real estate

What is a good DSCR for a commercial real estate loan?

Most commercial lenders require a minimum DSCR of 1.20x to 1.25x for stabilized commercial real estate loans. SBA 504 loans typically require 1.15x. Higher-risk property types or markets may require 1.30x or above. The specific threshold depends on the lender's risk appetite, property type, and market conditions.

How do lenders calculate DSCR for commercial loans?

DSCR is calculated by dividing Net Operating Income (NOI) by total annual debt service (principal + interest). NOI equals effective gross income minus operating expenses, excluding capital expenditures, depreciation, and debt service itself. Lenders typically stress-test by applying vacancy rates of 5-10% and verifying expense ratios against market benchmarks.

What is the difference between property-level and global DSCR?

Property-level DSCR measures only the subject property's cash flow against its debt. Global DSCR includes all income sources and all debt obligations of the borrower and guarantors across their entire portfolio. Most commercial lenders evaluate both, with global DSCR providing a fuller picture of repayment capacity.

What happens if DSCR falls below 1.0x?

A DSCR below 1.0x means the property's net operating income does not fully cover debt service — the borrower must supplement payments from other sources. This is a red flag for lenders and typically triggers loan covenant violations, increased monitoring, or restructuring. Most lenders will not originate a loan with a projected DSCR below 1.0x.

Going deeper on AI in underwriting? Our free playbook covers governance frameworks, six production use cases, regulatory expectations under SR 11-7, and an examiner readiness checklist. Read the AI-Assisted Underwriting Playbook.