What is financial spreading software?

Financial spreading software is underwriting software that reads a commercial borrower's tax returns and financial statements, extracts every figure the credit analyst would otherwise key by hand, and lands them in a standardized spread with a citation back to the source page. The category has been around for two decades. The reason it now needs a fresh definition is that the gap between template-based OCR spreaders and AI systems built for multi-entity commercial files has become wide enough to change which tool is the right buy.

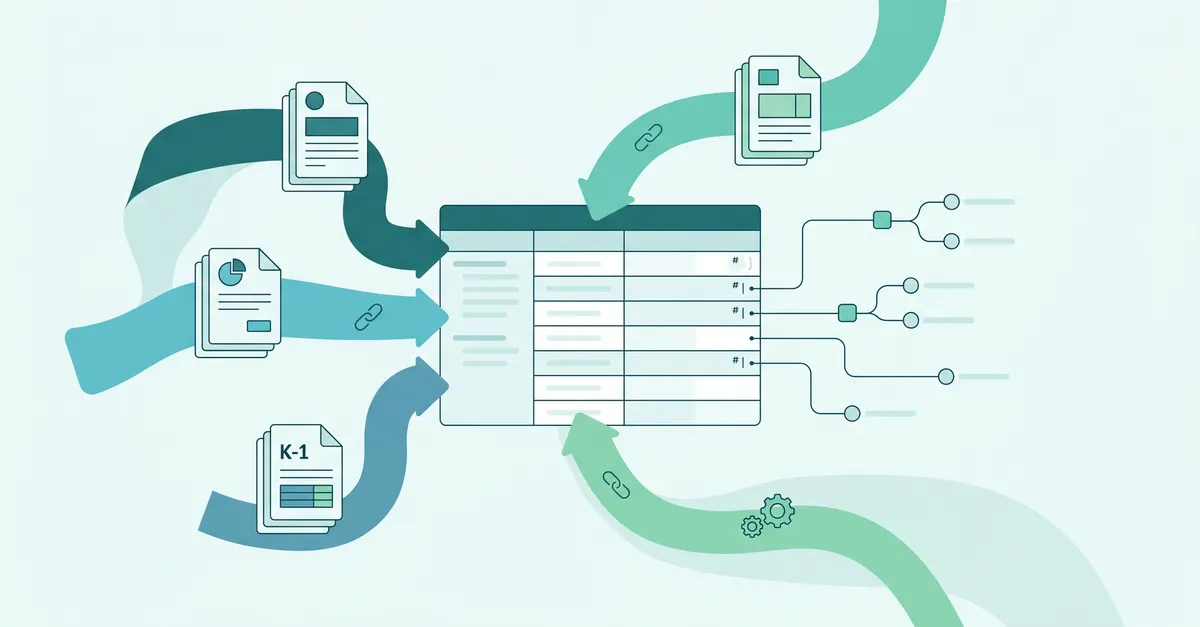

The core inputs are the returns commercial credit teams see every week: Forms 1040, 1065, 1120, and 1120-S, plus their supporting schedules, K-1s, Schedule C, Schedule E, financial statements, interim statements, bank statements, rent rolls, and personal financial statements. Bank-grade tools also handle amended returns, hand-annotated PDFs, and the mixed-quality scans that show up in the real world.

The output is a spread the underwriter can defend. Revenue, cost of goods, operating expense, officer compensation, depreciation, add-backs, debt service inputs, liquidity, and balance-sheet fields land in a template the bank chose, ready for ratio and covenant work. Every value carries a citation, an override marker if a human changed it, and an audit trail an examiner can walk without asking the analyst to explain their spreadsheet. For a plain-English definition of the broader category, see what is loan spreading software.

For community banks and regional banks under $10B, this matters because the bottleneck is analyst capacity, not policy design. A lean credit team still has to spread the same returns, trace the same ownership webs, and answer the same examiner questions as a larger institution. They just have fewer people to do it. The right workflow keeps the underwriter in charge. The system handles classification, extraction, cross-document reasoning, and first-pass calculations. The analyst verifies the output, adjusts treatment where judgment is required, and keeps the evidence trail showing what the system proposed and what changed.