The real problem in commercial underwriting is not that banks lack AI — it's that their analysts are already using ChatGPT on loan files without governance, audit trails, or data controls. Meanwhile, legacy LOS vendors are bolting AI features onto 20-year-old systems. The gap between what's being used and what's sanctioned is where the risk lives.

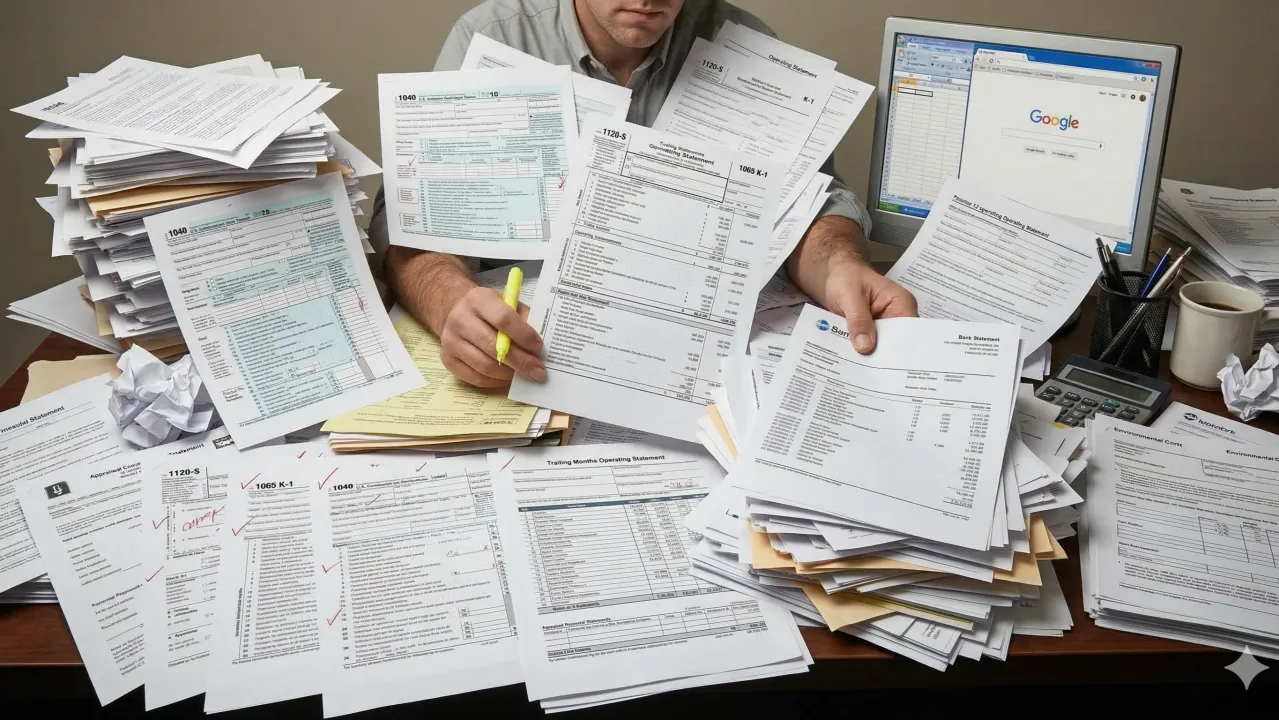

Here's the thing about commercial lending underwriting that most people outside the industry don't realize: it's mostly paper. Tax returns. Bank statements. Rent rolls. Appraisals. A community bank loan officer with twenty years of experience spends the majority of their day not making decisions, but gathering, organizing, and re-keying information from one document into another. The thinking is the job. The moving-stuff-around is what actually fills the day.

Into this world, the LOS vendors have arrived with their AI announcements. Every system now has an "AI-powered" something-or-other. A chatbot here. Some OCR there. It checks a box. The AI box. But the incentives are completely upside down. A legacy LOS vendor wants stability — which is a polite word for stasis. Every feature they add is a cost center. Their ideal state is one where nothing changes and the checks keep coming. Their customers want the exact opposite.

So the actual users route around the problem. They open ChatGPT in another tab. They paste in tax returns and ask it to calculate DSCR. Every loan officer becomes their own AI department. Zero controls. Zero audit trail. Zero consistency. Nobody is in charge.

The fundamental issue isn't that these systems lack AI features. It's that they weren't built for a world where AI exists. There's a difference between a tool that has AI and a tool that is AI-native. The gap between the two is roughly the same as the gap between a horse-drawn carriage with a motor strapped to the side and an automobile. The best AI in underwriting isn't the kind that replaces the human — it's the kind that knows when to help and when to shut up and let the human do their job.

Here's what's changed — and what genuinely wasn't feasible six months ago.

Every lender has their own process. First State Bank of Duluth does things differently than Central Savings of Topeka. This isn't a bug — it's the whole point. These processes encode decades of institutional knowledge, risk appetite, and hard-won lessons from deals that went sideways. And yet every SaaS product says the same thing: adapt your process to our software. The word they use is "best practices," but what they mean is "our practices, because we only built one workflow."

What if the software adapted to the lender? LLMs have gotten good enough — and cheap enough — that you can now take a lender's actual policy manual, their actual credit guidelines, and encode all of it into a system that enforces those rules automatically. Not a generic system. Their system.

At Aloan, this is exactly what we're building. We take a lender's underwriting policies and encode them into a rules engine that evaluates every deal against that institution's specific criteria. AI shows up where it earns its keep — document extraction, cross-referencing, policy enforcement — and stays quiet everywhere else. Guardrails. Audit trails. Self-improvement when analysts override a result. And education: a system that embodies institutional knowledge so well that a first-year hire has access to twenty years of expertise. That's not just efficiency. That's survival for institutions watching their experienced people retire.

Two years ago, building this required fifty ML engineers and a multi-million dollar budget. Only JPMorgan could play. That world is over. A five-person company — and Aloan is a five-person company — can now deploy systems that would have been the exclusive province of trillion-dollar institutions. The community bank with four branches, the credit union serving teachers, the specialty bridge lender — they're not too small anymore. The technology doesn't care how many branches you have. It cares about your process and your policies. And those, a two-hundred-million-dollar credit union has just as much as a two-hundred-billion-dollar bank.

Every lender is going to either build AI into their underwriting workflow or watch their competitors do it first. There is no third option. The choice is between software that was built around your policies, your risk appetite, your workflow — and software that was built for everyone and therefore built for no one.

The technology is finally ready.

Tim Diamond is the CTO and co-founder of Aloan (aloan.ai), an AI-native underwriting platform for community banks, credit unions, and specialty lenders.

FAQ: AI-native lending and underwriting software

What is AI-native lending software?

AI-native lending software is built from the ground up with artificial intelligence as the core architecture, not bolted onto a legacy system. This means AI handles document processing, financial analysis, risk detection, and memo generation as integrated capabilities — not add-on features layered on top of 20-year-old code. The distinction matters because AI-native platforms can adapt to new models and capabilities without requiring system replacements.

Why are LOS vendors struggling with AI?

Most loan origination systems were built 10-20 years ago as workflow and data management tools. Adding AI to these systems means bolting machine learning onto architectures designed for form-filling and routing. The result is limited AI capabilities constrained by the underlying system's data model, user interface, and processing pipeline. AI-native platforms start with the AI capability and build the workflow around it.

Should banks replace their LOS with AI software?

Not necessarily. The AI landscape changes every few months — an 18-month LOS replacement project locks you into last year's capabilities. A more effective approach is layering AI intelligence with existing systems so the institution can upgrade AI capabilities independently of its core lending infrastructure.