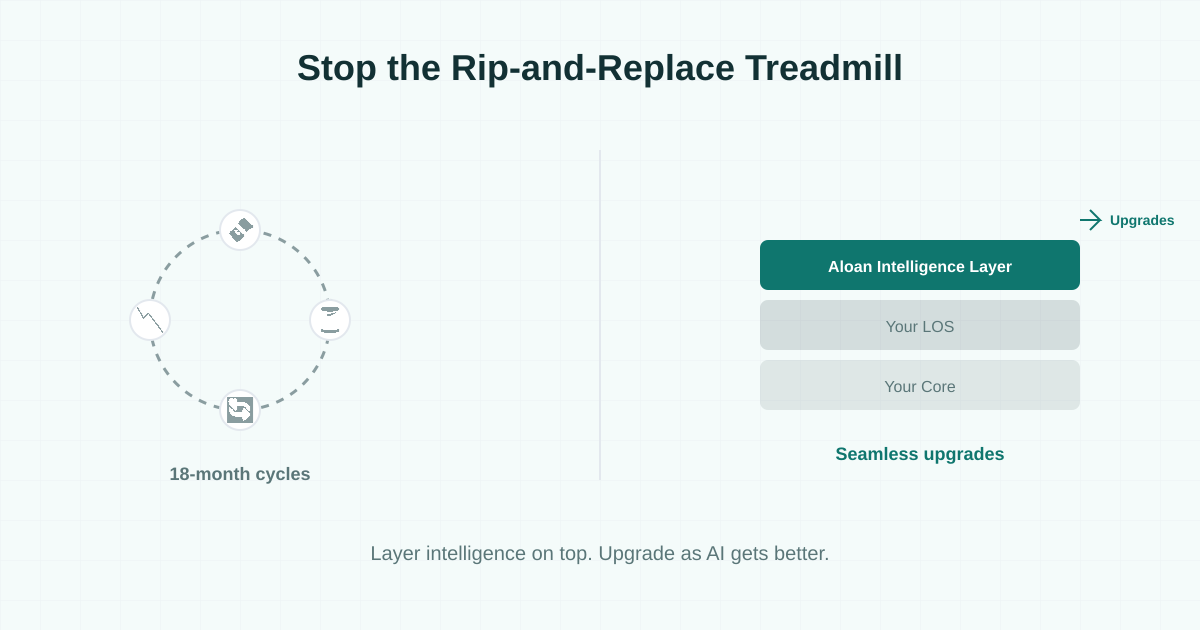

Banks should stop replacing their loan origination system every time AI capabilities improve. The AI landscape changes every few months. An 18-month LOS migration locks an institution into last year's technology. The alternative: layer AI intelligence with existing systems so upgrades happen without system replacements.

I talk to a lot of banks that are stuck.

They know the underwriting workflow is broken. They know their commercial team is buried in manual spreading, document chasing, and memo assembly. They've seen what's possible. They want to move.

But the vendors they're talking to all want the same thing: rip out your LOS and replace it with ours.

That's an 18-month project. Millions of dollars. Data migration. Retraining. Change management across every department that touches a loan. Core integration work that never goes as smoothly as the demo suggested.

And for what? To be locked into a new system that was built on last year's AI models.

The AI landscape is moving too fast for rip-and-replace.

Here's the part nobody's talking about. The models are changing every few months. Not small improvements — fundamental leaps in what's possible. What was state-of-the-art in document extraction six months ago is already behind. The credit memo generation capabilities that exist today didn't exist a year ago. Entity resolution, multi-document reasoning, policy-aware analysis — all of it is advancing at a pace that makes 18-month implementation timelines look insane.

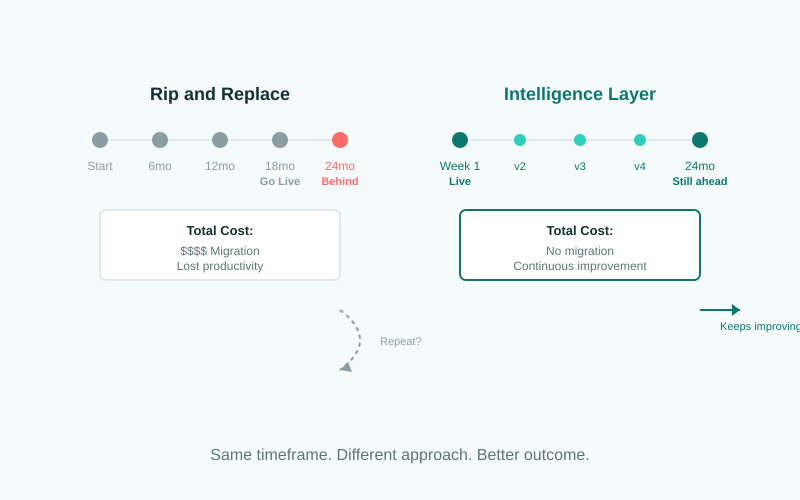

So you spend 18 months migrating to a new LOS. You finally go live. And the AI capabilities baked into that system are already a generation behind. What do you do? Rip and replace again?

That's not a technology strategy. That's a treadmill.

The banks that are going to win this cycle aren't the ones who made the biggest bet on one vendor. They're the ones who kept their existing infrastructure and layered intelligence on top — so when the models get better (and they will, fast), the upgrade is seamless. No migration. No retraining. No 18-month project.

What "working with existing systems" actually means.

When I say Aloan sits alongside your existing systems, I mean it literally. Your core stays. Your LOS stays. Your doc management stays. We don't touch any of it.

Here's what we handle:

Policy ingestion. Upload your credit policy documents — your DSCR floors, leverage limits, concentration thresholds, exception criteria. We read them and build your credit box. When the policy changes, upload the new version. Done. No vendor configuration call. No ticket.

Document collection. Borrower gets a portal. They upload their tax returns, financials, entity docs, bank statements. The system reads what's there, identifies what's missing, and generates specific document requests. "We need the 2024 Form 1065 for Pine Street Partners LP, referenced on the Schedule K-1 from Smith Holdings LLC." Not a generic checklist. A targeted ask based on what we've already read.

Underwriting analysis. Documents come in, structured spreads come out. Every number traced to the source document and page. Multi-entity ownership trees built automatically. Global cash flow calculated across the full entity structure. Exceptions flagged against your actual policy — not generic benchmarks.

Credit memo generation. A draft credit memo with your borrower's actual story. Not a data dump. Exceptions called out. Mitigating factors surfaced. Risk flags explained. Your underwriter reviews it, edits it, makes it theirs. Their name on it. Their judgment. We just gave them a 40-hour head start.

All of that runs without replacing a single system you're already using. Live in as little as a week. Not a year. A week. For a deeper look at how AI-native commercial loan origination software compares with legacy LOS platforms across the four automation areas, see the category page.

The cost of being wrong about your vendor is about to go up.

Think about the next 12 to 24 months. A bank that ripped and replaced their LOS in January is now locked in. The contract is signed. The migration happened. The team is trained on the new system.

When the next generation of AI capabilities drops — and it will — they're stuck waiting for their vendor to catch up. Or they're starting the rip-and-replace cycle all over again.

Now think about a bank that kept their existing LOS and layered Aloan on top. Same week the new models drop, the analysis gets better. The spreading gets more accurate. The memo generation gets sharper. The document understanding deepens. Nothing changes in their workflow. Nothing changes in their core systems. The intelligence just gets better.

That's not a small difference. Over 24 months of AI advancement, that's the difference between riding the wave and drowning in implementation cycles.

Every rip-and-replace you do is six figures minimum. Often seven. Plus the hidden costs — productivity loss during migration, deals that slip through during the transition, the three months where nobody trusts the new system yet. Stack two of those in 24 months and you've spent more on switching than you would have spent in five years of running a system that just upgrades underneath you. According to Cornerstone Advisors' annual banking technology survey, the average core/LOS system replacement takes 12-18 months and costs between $500,000 and $5 million depending on institution size.

| Factor | Rip-and-Replace LOS | AI-Native Underwriting Approach |

|---|---|---|

| Implementation time | 12-18 months | 4-6 weeks |

| Cost | Six to seven figures | Fraction of LOS replacement |

| AI upgrade path | Locked to vendor's roadmap | Independent — upgrade AI without system change |

| Vendor lock-in risk | High — data migration required to switch | Low — AI layer is independent of core LOS |

| Change management | Full staff retraining | Minimal — works alongside existing workflow |

| Risk during transition | High — parallel processing period | Low — additive, not replacement |

The LOS vendors don't want you to think about this.

Of course they don't. Their business model depends on lock-in. They want to be your system of record because once they are, switching costs keep you paying forever.

We don't need to be your system of record. If your LOS works, keep it, and Aloan makes it work harder for your underwriting team. If you're launching a lending program with nothing to replace, Aloan can be your system of record from day one. The difference is we never make replacement the price of admission.

Your LOS handles what it handles. Your core does what it does. We handle the part that's actually broken — the manual work between document receipt and credit decision. That's the gap. That's where the weeks go. And that's what we built Aloan to fix.

The systems you already have are fine. The workflow connecting them is the problem.

You don't need a new house. You need a better engine.

Mitch Barnard is a co-founder of Aloan (aloan.ai), an AI-native underwriting platform for community banks, credit unions, and specialty lenders.

FAQ: LOS replacement and AI-native underwriting

How long does it take to replace a loan origination system?

A full LOS replacement typically takes 12-18 months from vendor selection to go-live, with costs ranging from six figures to seven figures depending on institution size and complexity. This includes data migration, workflow reconfiguration, staff training, and parallel processing periods. During this time, the institution operates on both old and new systems.

Can AI work with my existing loan origination system?

Yes. AI-native underwriting platforms like Aloan work with existing LOS infrastructure and handle document processing, financial spreading, risk detection, and credit memo generation independently. The AI reads the same documents your team does and produces structured output that integrates with your existing workflow — without requiring a system migration.

What is AI-native underwriting for commercial lending?

AI-native underwriting is an intelligence layer that works with an institution's existing lending infrastructure. Rather than replacing the LOS, it automates the analysis work — document collection, financial spreading, risk flagging, and memo generation — and delivers structured results into the existing workflow. This approach allows banks to upgrade AI capabilities independently of their core systems.