Commercial lending is fundamentally an information logistics problem, not an intelligence problem. Loan decisions that could take minutes take weeks because the bottleneck is manual document collection, manual financial spreading, and manual verification — not the credit judgment itself. Solving the logistics unlocks the speed.

Consumer lending solved the speed problem decades ago. The entire industry compressed a borrower's financial history into a three-digit number. A credit score is a logistics shortcut—it eliminates the need to collect, verify, and interpret hundreds of pages of documents for every single loan.

Commercial lending never got that shortcut. And the result is that loan decisions that could take minutes still take weeks or months. According to the CSBS Community Banking Research, the median commercial loan takes 30-60 days from application to decision at community banks — with the majority of that time spent on document collection and data preparation, not credit analysis.

The Document Collection Challenge

Banks request extensive documentation for commercial deals: three years of tax returns, personal financial statements, bank statements, debt schedules—and conditional items like environmental reports, appraisals, or lease agreements depending on the collateral.

On the surface, this looks standardized. Every bank has a checklist. But there's enormous variation in what actually gets collected. One loan officer demands audited financials for a $500K deal. Another closes a similar deal with tax returns and a conversation.

The problem isn't that lenders don't know what they need. It's that getting it all in the door, organized, and cross-referenced is a logistics operation—not a credit decision.

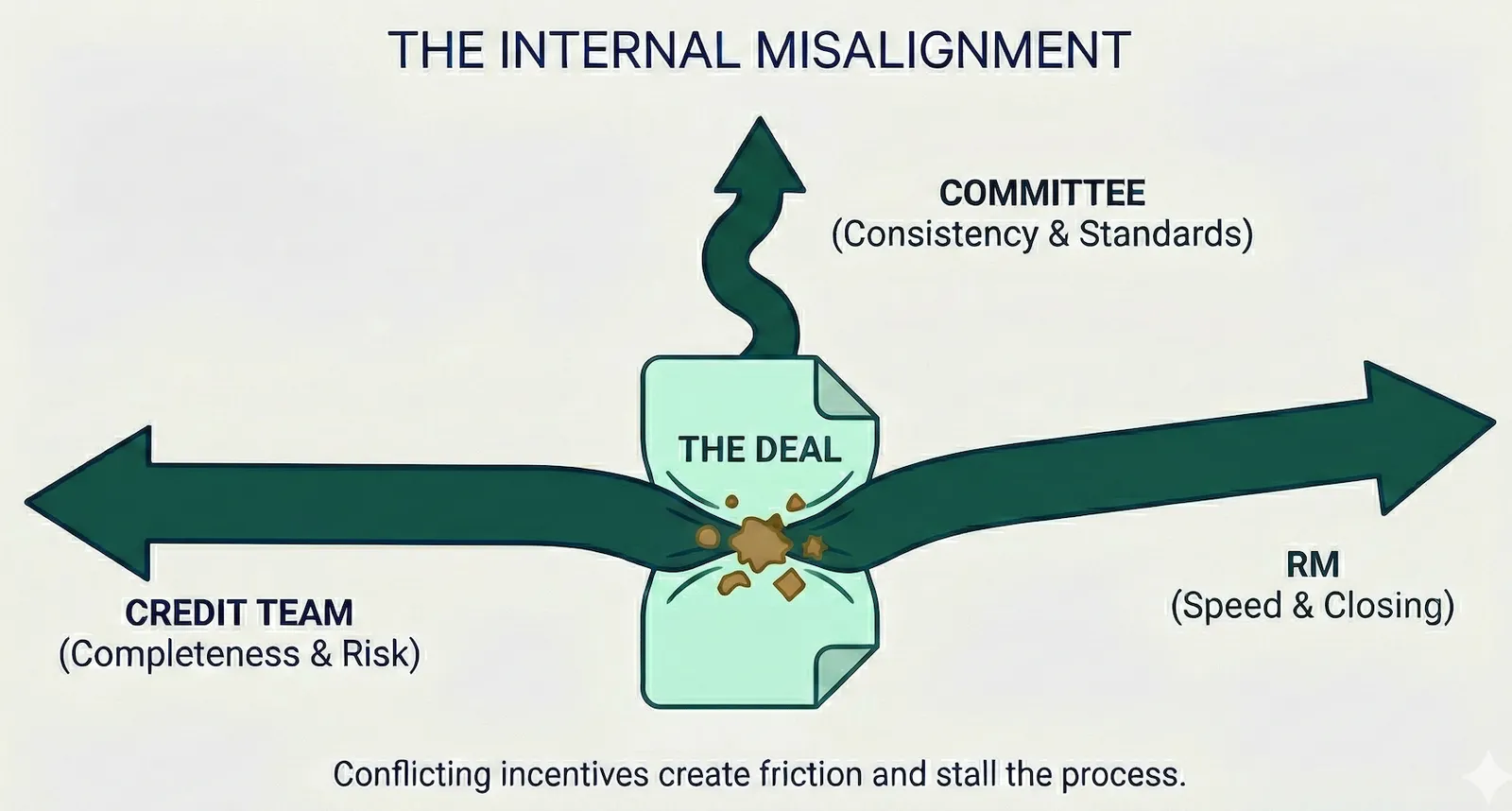

Three Groups, Conflicting Incentives

Every commercial deal passes through at least three groups with fundamentally different priorities:

Relationship Managers

Prioritize speed and deal closure. They're compensated on volume and relationships—every day a deal sits in the pipeline is a day it might walk to another lender.

Credit Teams

Demand thorough documentation and analysis. Their job is to identify risk, and incomplete packages are their biggest headache.

Credit Committees

Enforce portfolio-level consistency. They need to see that similar deals are being underwritten the same way—and that nothing was missed.

These groups aren't misaligned because anyone is doing their job wrong. They're misaligned because the information they need moves through the same bottleneck: manual document collection, manual spreading, manual verification.

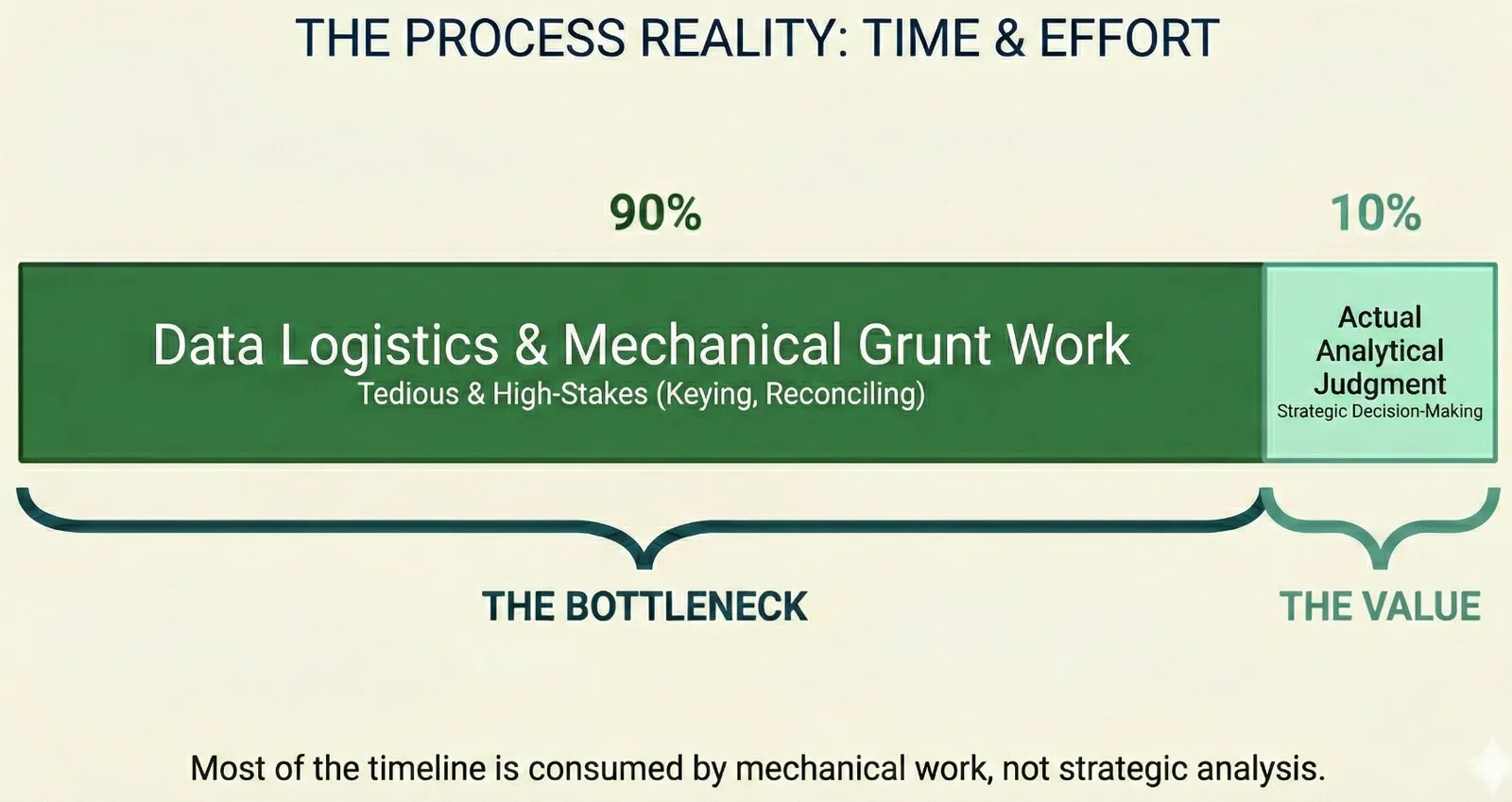

"Six weeks of calendar time. Much less of actual judgment."

The Hidden Work

Ask an analyst where their time goes and the answer is almost never "evaluating credit quality." Most of it is mechanical: keying numbers from tax returns into spreadsheets, reconciling discrepancies between P&Ls and bank deposits, cross-referencing one document against another to make sure the story holds together.

This is skilled work—it requires knowing what to look for and where the numbers should tie out. But it's not judgment work. It's verification and data entry work that happens to require domain knowledge.

The bottleneck in commercial lending isn't intelligence. It's logistics. Getting the right numbers, from the right documents, into the right format, with the right audit trail—so that someone with real underwriting expertise can actually make a decision.

Speed Is a Competitive Advantage

Community banks with flatter organizational structures close deals faster. Not because they cut corners on credit—but because there are fewer handoffs, fewer queues, and fewer layers of review.

Borrowers notice. They'll accept higher rates for quicker approvals because speed creates tangible business value. A contractor waiting on equipment financing isn't comparing basis points—they're comparing how many weeks of revenue they'll lose while the loan committee meets.

The lenders winning deals aren't necessarily offering better terms. They're offering faster answers. And right now, that speed advantage comes from organizational structure rather than technology—which means it doesn't scale.

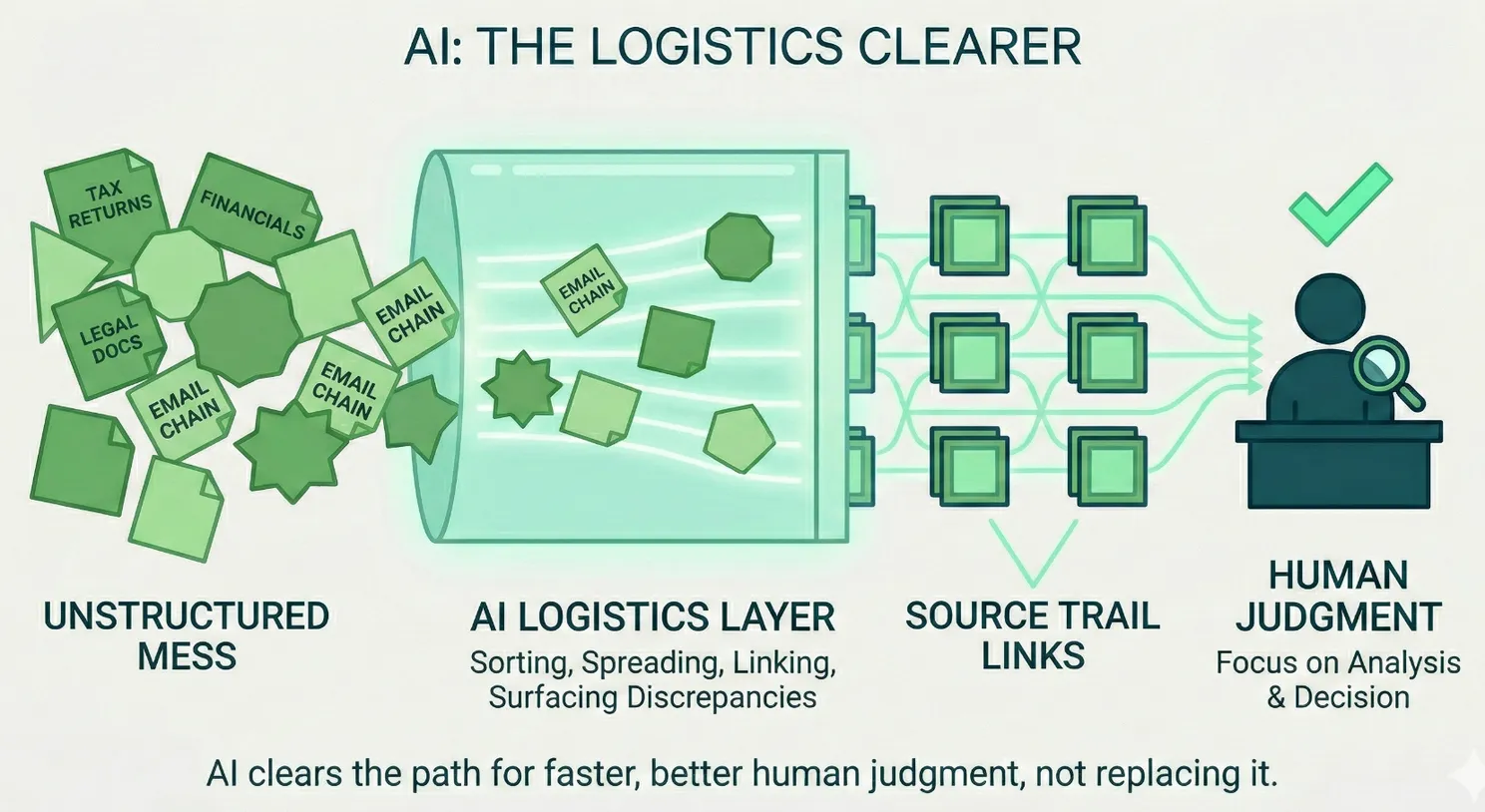

What Technology Actually Solves

AI isn't going to replace underwriters. The judgment calls in commercial lending—how to weight a borrower's character, whether an industry trend changes the risk profile, what a declining margin really means for this specific business—those require human expertise and always will.

But the mechanical work that surrounds those judgment calls? That's a different story entirely.

Financial Spreading

Extracting numbers from tax returns and financial statements directly—no manual keying, no transposition errors, no three-hour spreadsheet sessions.

Cross-Document Validation

Surfacing discrepancies between documents ranked by materiality. When the P&L says one thing and the bank statements say another, the system flags it—so the analyst focuses on what matters instead of hunting for what's wrong.

Source Traceability

Every number links back to the specific page of the source document. When the credit committee asks "where did this number come from?"—there's an instant answer, not a 20-minute document hunt.

"The underwriter is still the underwriter. But instead of spending three hours keying numbers, they're analyzing credit quality."

Making Speed Scalable

Today, fast underwriting depends on individual experience. A veteran analyst who's seen a thousand deals can spread financials quickly because they know where to look. But that speed lives in one person's head—and it leaves when they do.

The right infrastructure makes speed a property of the system, not the individual. Human judgment stays essential. But the logistics work that consumes most of the timeline—collecting, organizing, verifying, formatting—becomes automated infrastructure that works the same way every time, for every deal, regardless of who's running the file.

Building the case for AI in your lending shop? Our free playbook covers governance frameworks, six production use cases, what examiners actually ask, and a 30/60/90-day implementation roadmap. Read the AI-Assisted Underwriting Playbook.

FAQ: Commercial lending information logistics

Why do commercial loans take so long to close?

Commercial loan closings are delayed primarily by information logistics — manual document collection, back-and-forth with borrowers for missing items, manual data entry from PDFs into spreadsheets, and verification across multiple entity structures. The credit decision itself often takes minutes; the data gathering and preparation takes weeks. Industry surveys indicate the median commercial loan takes 30-60 days from application to decision.

What is information logistics in commercial lending?

Information logistics refers to the process of collecting, organizing, verifying, and routing the documents and data needed for a commercial loan decision. This includes tax returns, financial statements, rent rolls, entity documents, insurance certificates, and environmental reports — often 500-1,000+ pages per deal across multiple borrower entities.

How can banks speed up commercial loan processing?

The highest-impact improvement is automating information logistics: AI-powered document collection that tracks what's received and what's missing, automated extraction and spreading of financial data from tax returns and statements, and intelligent routing that delivers organized data to underwriters ready for analysis. This eliminates the manual bottleneck without changing the credit judgment process.